New Overseas Direct Investment (ODI) / Overseas Investment (OI) Regime under the FEMA

Introduction

Overseas investments by persons resident in India enhance the scale and scope of business operations of Indian entrepreneurs by providing global opportunities for growth. Such ventures through easier access to technology, research and development, a wider global market and reduced cost of capital along with other benefits increase the competitiveness of Indian entities and boost their brand value. These overseas investments are also important drivers of foreign trade and technology transfer thus boosting domestic employment, investment and growth through such interlinkages.

In keeping with the spirit of liberalisation and to promote ease of doing business, the Central Government and the Reserve Bank of India have been progressively simplifying the procedures and rationalising the rules and regulations under the Foreign Exchange Management Act, 1999.

It is stated that the new regime simplifies the existing framework for overseas investment by persons resident in India to cover wider economic activity and significantly reduces the need for seeking specific approvals. This will reduce the compliance burden and associated compliance costs.

Some of the significant changes brought about through the new rules and regulations are summarised below:

(i) enhanced clarity with respect to various definitions;

(ii) introduction of the concept of “strategic sector”;

(iii) dispensing with the requirement of approval for:

- deferred payment of consideration;

- investment/disinvestment by persons resident in India under investigation by any investigative agency/regulatory body;

- issuance of corporate guarantees to or on behalf of second or subsequent level step down subsidiary (SDS);

- write-off on account of disinvestment;

(iv) introduction of “Late Submission Fee (LSF)” for reporting delays.

Relevant Rules, Regulations and Directions for the Overseas Investment and Overseas Direct Investment (ODI) – these all collectively will be referred to as “new regime”

|

Rules/Regulations/Directions |

Purpose / Scope |

|

Foreign Exchange Management (Overseas Investment) Rules, 2022 |

Provides Rules related to Non-Debt Instruments related transactions |

|

Foreign Exchange Management (Overseas Investment) Regulations, 2022 |

Provides Regulations related to Debt Instruments related transactions |

|

Foreign Exchange Management (Overseas Investment) Directions, 2022 |

Provides comprehensive directions regarding Rules and Regulations as stated to the above |

|

Master Direction – Reporting under Foreign Exchange Management Act, 1999 (Updated as on August 22, 2022) |

Provides directions with respect to reporting requirements of Overseas Investments |

|

Master Direction - Liberalised Remittance Scheme (LRS) (Updated as on August 24, 2022) |

Provides updated directions with respect to LRS by incorporating above Rules and Regulations |

Some of the key highlights to the above rules / regulations / directions are discussed as under:

1. Overseas Direct Investment and Overseas Portfolio Investment - defined

“Overseas Direct Investment” or “ODI” means investment by way of

- acquisition of unlisted equity capital of a foreign entity, or

- subscription as a part of the memorandum of association of a foreign entity, or

- investment in 10%, or more of the paid-up equity capital of a listed foreign entity or

- investment with control where investment is less than 10%. of the paid-up equity capital of a listed foreign entity;

It is also provided / clarified that where an investment by a person resident in India in the equity capital of a foreign entity is classified as ODI, such investment shall continue to be treated as ODI even if the investment falls to a level below ten per cent. of the paid-up equity capital or such person loses control in the foreign entity;

“Overseas Portfolio Investment” or “OPI” means investment, other than ODI, in foreign securities, but not in any unlisted debt instruments or any security issued by a person resident in India who is not in an IFSC

It is also provided / clarified that OPI by a person resident in India in the equity capital of a listed entity, even after its delisting shall continue to be treated as OPI until any further investment is made in the entity.

2. Continuity of existing ODI Investments:

Rule 6 of the Foreign Exchange Management (Overseas Investment) Rules, 2022 provides that Any investment or financial commitment outside India made in accordance with the Act or the rules or regulations made thereunder and held as on the date of publication of these rules in the Official Gazette, shall be deemed to have been made under these rules and the Foreign Exchange Management (Overseas Investment) Regulations, 2022.

3. Bona fide Business Activity:

It is specifically stated that any investment made outside India by a person resident in India shall be made in a foreign entity engaged in a bona fide business activity, directly or through step down subsidiary or the special-purpose vehicle, subject to the limits and the conditions laid down in these rules and the said regulations. It is also clarified that “bonafide business activity” shall mean any business activity permissible under any law in force in India and the host country or host jurisdiction, as the case may be.

4. No Objection Certificate (NoC):

Rule 10 provides that Any person resident in India who,

(i) has an account appearing as a non-performing asset; or

(ii) is classified as a wilful defaulter by any bank; or

(iii) ) is under investigation by a financial service regulator or by investigative agencies in India, namely, the Central Bureau of Investigation or Directorate of Enforcement or Serious Frauds Investigation Office,

shall, before making any financial commitment or undertaking disinvestment under these rules or the Foreign Exchange Management (Overseas Investment) Regulations, 2022, obtain a No Objection Certificate from the lender bank or regulatory body or investigative agency by making an application in writing to such bank or regulatory body or investigative agency concerned:

However, where the lender bank or regulatory body or investigative agency concerned fails to furnish the certificate within 60 days from the date of receipt of such application, it may be presumed that there was no objection to the proposed transaction.

Here, it is note worthy to state that “financial commitment” is also defined under the Rules, which provides that “financial commitment” means the aggregate amount of investment made by a person resident in India by way of Overseas Direct Investment, debt other than Overseas Portfolio Investment in a foreign entity or entities in which the Overseas Direct Investment is made and shall include the non-fund-based facilities extended by such person to or on behalf of such foreign entity or entities;

5. General Restrictions and Prohibition:

Rule 19 contains restrictions and prohibitions w.r.t. ODI transaction.

Restrictions with respect to nature of business

Subrule 1 provides that unless otherwise provided in the Act or these rules, no person resident in India shall make ODI in a foreign entity engaged in

(a) real estate activity;

(b) gambling in any form; and

(c) dealing with financial products linked to the Indian rupee without specific approval of the Reserve Bank.

Explanation.– For the purposes of this sub-rule, the expression "real estate activity" means buying and selling of real estate or trading in Transferable Development Rights but does not include the development of townships, construction of residential or commercial premises, roads or bridges for selling or leasing.

Restriction with respect to ODI in start ups

Any ODI in start-ups recognised under the laws of the host country or host jurisdiction as the case may be, shall be made by an Indian entity only from the internal accruals whether from the Indian entity or group or associate companies in India and in case of resident individuals, from own funds of such an individual.

Restrictions with respect to round tripping or layer of subsidiaries

No person resident in India shall make financial commitment in a foreign entity that has invested or invests into India, at the time of making such financial commitment or at any time thereafter, either directly or indirectly, resulting in a structure with more than two layers of subsidiaries:

However, above restrictions shall not be applicable to the;

(a) a banking company as defined in clause (c) of section 5 of the Banking Regulation Act, 1949 (10 of 1949);

(b) a non-banking financial company as defined in clause (f) of section 45-I of the Reserve Bank of India Act, 1934 (2 of 1934) which is registered with the Reserve Bank and considered as systematically important non-banking financial company by the Reserve Bank;

(c) an insurance company being a company which carries on the business of insurance in accordance with provisions of the Insurance Act, 1938 (4 of 1938) and the Insurance Regulatory and Development Authority Act, 1999 (41 of 1999); and

(d) a Government company referred to in clause (45) of section 2 of the Companies Act, 2013 (18 of 2013).

6. Provisions related to the acquisition or transfer of immovable property outside India:

Rule 21 contains the detailed provisions relating to the acquisition and transfer of immovable property by the person resident in India. The said rules are reproduced as under:

21. Restriction on acquisition or transfer of immovable property outside India.–

(1) Save as otherwise provided in the Act or this rule, no person resident in India shall acquire or transfer any immovable property situated outside India without general or special permission of the Reserve Bank:

Provided that nothing contained in this rule shall apply to a property–

(i) held by a person resident in India who is a national of a foreign State;

(ii) acquired by a person resident in India on or before the 8th day of July, 1947 and continued to be held by such person with the permission of the Reserve Bank;

(iii) acquired by a person resident in India on a lease not exceeding five years.

(2) Notwithstanding anything contained in sub-rule (1)–

(i) a person resident in India may acquire immovable property outside India by way of inheritance or gift or purchase from a person resident in India who has acquired such property as per the foreign exchange provisions in force at the time of such acquisition;

(ii) a person resident in India may acquire immovable property outside India from a person resident outside India–

(a) by way of inheritance;

(b) by way of purchase out of foreign exchange held in RFC account;

(c) by way of purchase out of the remittances sent under the Liberalised Remittance Scheme instituted by the Reserve Bank: Provided that such remittances under the Liberalised Remittance Scheme may be consolidated in respect of relatives if such relatives, being persons resident in India, comply with the terms and conditions of the Scheme;

(d) jointly with a relative who is a person resident outside India;

(e) out of the income or sale proceeds of the assets, other than ODI, acquired overseas under the provisions of the Act;

(iii) an Indian entity having an overseas office may acquire immovable property outside India for the business and residential purposes of its staff, as per the directions issued by the Reserve Bank from time to time;

(iv) a person resident in India who has acquired any immovable property outside India in accordance with the foreign exchange provisions in force at the time of such acquisition may–

(a) transfer such property by way of gift to a person resident in India who is eligible to acquire such property under these rules or by way of sale;

(b) create a charge on such property in accordance with the Act or the rules or regulations made thereunder or directions issued by the Reserve Bank from time to time.

(3) The holding of any investment in immovable property or transfer thereof in any manner shall not be permitted if the initial investment in immovable property was not permitted under the Act.

7. Overseas Investment by resident individual:

Schedule III of the Rules contains the provisions relating to the Manner of making Overseas Investment by resident individual.

Any resident individual may make ODI by way of investment in equity capital or OPI in the manner provided in this Schedule and unless otherwise provided hereunder, shall be subject to the overall ceiling under the Liberalised Remittance Scheme of the Reserve Bank.

A resident individual may make or hold Overseas Investment by way of ODI in an operating foreign entity not engaged in financial services activity and which does not have subsidiary or step down subsidiary where the resident individual has control in the foreign entity.

However, restrictions regarding the financial services activity or subsidiary or step down subsidiary shall not apply in case where ODI or OPI, as the case may be, by way of

- inheritance;

- acquisition of sweat equity shares;

- acquisition of minimum qualification shares issued for holding a management post in a a. foreign entity;

- acquisition of shares or interest under Employee Stock Ownership Plan or Employee Benefits Scheme:

It is also clarified that a foreign entity will be considered to be engaged in the business of financial services activity if it undertakes an activity, which if carried out by an entity in India, requires registration with or is regulated by a financial sector regulator in India.

8. Acquisition of shares or interest under Employee Stock Ownership Plan or Employee Benefits Scheme or sweat equity shares by the resident individual:

A resident individual, who is an employee or a director of an office in India or branch of an overseas entity or a subsidiary in India of an overseas entity or of an Indian entity in which the overseas entity has direct or indirect equity holding, may acquire, without limit, shares or interest under Employee Stock Ownership Plan or Employee Benefits Scheme or sweat equity shares offered by such overseas entity, provided that the issue of Employee Stock Ownership Plan or Employee Benefits Scheme are offered by the issuing overseas entity globally on a uniform basis.

9. ODI by Registered Trust or Society:

Registered Trust or a registered Society engaged in the educational sector or which has set up hospitals in India may make ODI in a foreign entity with the prior approval of the Reserve Bank, subject to the following conditions

- the foreign entity is engaged in the same sector that the Indian Trust or Society is engaged in

- the Trust or the Society, as the case may be, should have been in existence for at least three financial years before the year in which such investment is being made

- such investment have the approval of the trustees in case of a Trust and the governing body or council or managing or executive committee in case of a Society

- in case the Trust or the Society require special licence or permission either from the Ministry of Home Affairs, Central Government or from the relevant local authority, as the case may be, the special licence or permission has been obtained and submitted to the designated AD bank.

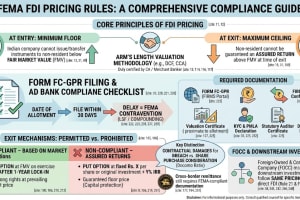

10. Pricing Guidelines:

The issue or transfer of equity capital of a foreign entity

- from a person resident outside India or

- a person resident in India to a person resident in India who is eligible to make such investment or

- from a person resident in India to a person resident outside India

shall be subject to a price arrived on an arm’s length basis.

The AD bank, before facilitating a transaction, shall ensure compliance with arm’s length pricing taking into consideration the valuation as per any internationally accepted pricing methodology for valuation.

11. Modes of Payment:

A person resident in India making Overseas Investment may make payment

by remittance made through banking channels;

from funds held in an account maintained in accordance with the provisions of the Act;

by swap of securities;

by using the proceeds of American Depository Receipts or Global Depositary Receipts or stock-swap of such receipts or external commercial borrowings raised in accordance with the provisions of the Act and the rules and regulations made thereunder for making ODI or financial commitment by way of debt by an Indian entity.

12. Reporting requirements for Overseas Investment:

|

Form Name |

Relevant for |

Time limit |

|

Form FC |

Information relating to financial commitment including ODI, restructuring and disinvestment by Indian entities (as defined under the OI Rules) and resident individuals, as applicable |

- financial commitment (whether it is reckoned towards the financial commitment limit or not), at the time of sending outward remittance or making a financial commitment, whichever is earlier;

- disinvestment within 30 days of receipt of disinvestment proceeds;

- restructuring within 30 days from the date of such restructuring. |

|

Form OPI |

A person resident in India (other than a resident individual) making any Overseas Portfolio Investment (OPI) or transferring such OPI by way of sale |

Report such investment or transfer of investment within sixty days from the end of the half-year in which such investment or transfer is made as of September or March-end |

|

Form APR |

A person resident in India acquiring equity capital in a foreign entity which is reckoned as ODI, shall submit an Annual Performance Report (APR) with respect to each foreign entity |

every year by 31st December and where the accounting year of such foreign entity ends on 31st December, the APR shall be submitted by 31st December of the next year.

However, reporting is not applicable where a person resident in India is holding less than 10 per cent. of the equity capital without control in the foreign entity and there is no other financial commitment other than by way of equity capital; or a foreign entity is under liquidation. |

|

Form FLA |

This form is required to be submitted directly by all the Indian entities which have made ODI in the previous year(s) including the current year, to the Department of Statistics and Information Management (DSIM), Reserve Bank of India. The form FLA is available on RBI’s website viz. www.flair.rbi.org.in |

to be reported by July 15th of every year |

13. Delay in Reporting and Late Submission Fees:

Delay in Reporting

In case a person resident in India has made a delay in filing/submitting the requisite form/return/document, such person may file/submit the requisite form/return/ document, etc. and pay the Late Submission Fee (LSF) through the designated AD bank in accordance with regulation 11 of OI Regulations.

The LSF for delay in reporting of overseas investment related transactions shall be calculated as per the following matrix:

|

Sr. No. |

Type of Reporting delays |

LSF Amount (INR) |

|

1 |

Form ODI Part-II/ APR, FLA Returns, Form OPI, evidence of investment or any other return which does not capture flows or any other periodical reporting |

7500 |

|

2 |

Form ODI-Part I, Form ODI-Part III, Form FC, or any other return which captures flows or returns which capture reporting of non-fund based transactions or any other transactional reporting |

[7500 + (0.025% × A × n)] |

Notes:

“n” is the number of years of delay in submission rounded-upwards to the nearest month and expressed up to 2 decimal points.

“A” is the amount involved in the delayed reporting.

- LSF amount is per return.

- Maximum LSF amount will be limited to 100 per cent of ‘A’ and will be rounded upwards to the nearest hundred.

- Where an advice has been issued for payment of LSF and such LSF is not paid within 30 days, such advice shall be considered as null and void and any LSF received beyond this period shall not be accepted. If the applicant subsequently approaches for payment of LSF for the same delayed reporting, the date of receipt of such application shall be treated as the reference date for the purpose of calculation of LSF.

- The option of LSF shall be available up to three years from the due date of reporting/submission under OI Regulations. The option of LSF shall also be available for delayed reporting/submissions under the Notification No. FEMA 120/2004-RB and earlier corresponding regulations, up to three years from the date of notification of OI Regulations.

- In case a person resident in India responsible for submitting the evidence of investment or filing any forms/returns/reports, etc. as per OI Regulations/earlier corresponding regulations, neither makes such submission/filing within the specified time nor makes such submission/filing along with LSF as provided in regulation 11 of OI Regulations, such person shall be liable for penal action under the provisions of FEMA, 1999.

- The LSF may be paid by way of a demand draft drawn in favour of “Reserve Bank of India” and payable at the Regional Office concerned (in accordance with UIN mapping given in the table below).

|

Sr.No |

UIN with prefix |

UIN mapped to |

|

1. |

AH |

RO Ahmedabad |

|

2. |

BG |

RO Bengaluru |

|

3. |

BL or BY or PJ |

RO Mumbai |

|

4. |

BN or CA or GA or GH |

RO Kolkata |

|

5. |

CG or JM or JR or KA or ND or PT or WR |

RO New Delhi |

|

6. |

HY |

RO Hyderabad |

|

7. |

KO or MA |

RO Chennai |

- In a case if person not eligible or qualify to pay LSF then he may opt for the compounding.

SIMILAR ARTICLES