Permanent Establishment: Risk Analysis and Advisory for Multinational Enterprises

Permanent Establishment: Risk Analysis and Advisory for Multinational Enterprises

1. Introduction

As multinational enterprises expand their global footprints, the operational landscape is becoming increasingly complex. In an era where technological advancements allow companies to reach global markets without establishing a traditional brick-and-mortar footprint, the boundaries of cross-border taxation have blurred. What used to be a straightforward exercise in identifying physical branches or factories has transformed into a highly nuanced evaluation of unintended tax liabilities.

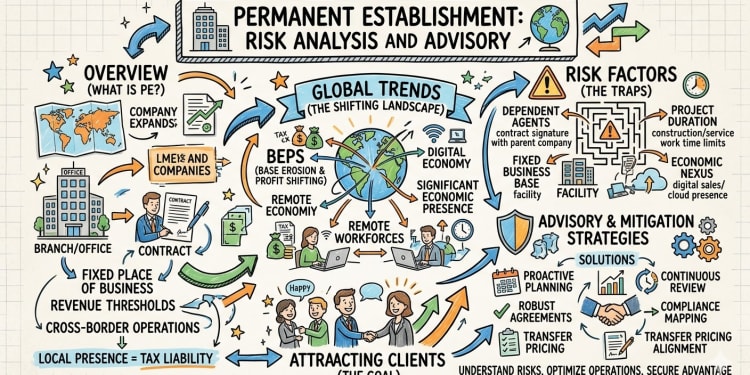

At the heart of this international tax architecture is the concept of a Permanent Establishment (PE). Under Article 5 of the OECD and UN Model Tax Conventions, a PE is fundamentally defined as a "fixed place of business through which the business of an enterprise is wholly or partly carried on". The determination relies on three core conditions: the existence of a place of business (such as premises, machinery, or equipment), its "fixed" nature implying a distinct geographical location with a degree of permanence, and the carrying out of the enterprise's business through that location by dependent personnel. If a PE is constituted, the source country gains the right to tax the business profits of the foreign enterprise to the extent they are attributable to that local establishment.

2. The Shifting Global Landscape (Global Trends)

The traditional tax rules, designed nearly a century ago for an industrial economy, have been placed under immense strain by recent global trends. Three primary shifts are currently redefining PE risk:

- The Impact of BEPS: Driven by the G20 and OECD, the Base Erosion and Profit Shifting (BEPS) project aims to align the taxation of profits with the location of actual economic activity and value creation. Specifically, BEPS Action 7 was introduced to prevent the artificial avoidance of PE status. It targets structures such as commissionaire arrangements and the fragmentation of business activities, ensuring that companies cannot circumvent PE thresholds by claiming their operations are merely "preparatory or auxiliary".

- The Digital Economy & Significant Economic Presence: Digitalisation allows enterprises to generate substantial profits in a market jurisdiction with little to no physical mass. To combat this, the concept of Significant Economic Presence (SEP) has emerged through BEPS Action 1 initiatives. Countries like India and Israel have pioneered domestic laws where tax nexus is triggered by digital factors—such as localized revenue thresholds, user volume, or the systemic soliciting of business through digital means—irrespective of a physical office.

- Remote Cross-Border Workforces: The post-pandemic normalisation of teleworking has triggered new PE exposures. The 2025 update to the OECD Model Tax Convention explicitly addresses cross-border remote work, noting that a home office may constitute a PE if an individual works there for at least 50% of their time, provided there is a commercial rationale for the physical presence in that jurisdiction and the enterprise requires or benefits from that arrangement.

3. Core Risk Analysis

Unintended PE creation is a pervasive risk that can subject a multinational to double taxation, stringent penalties, and rigorous audits. Common traps that enterprises frequently fall into include:

- Fixed Place via Home Offices and Client Sites: A place of business does not need to be legally owned or rented by the foreign enterprise; it simply must be "at its disposal". For example, in the Danish Aska Gmbh case, a Scandinavian sales manager's use of a home office for recurring administrative work constituted a fixed-place PE for his German employer, as the activities were core to the business and not merely preparatory. Similarly, the OECD highlights that a painter who spends three days a week for two years working in a client's large office building establishes a PE at that client site.

- Server Locations: Operating a computer server in a foreign jurisdiction can trigger a PE if the server is located at a distinct place for a sufficient period and is owned or leased by the enterprise. For instance, an e-tailer hosting a website on an independent Internet Service Provider (ISP) does not create a PE, as the server is not at the enterprise's disposal. However, if that same enterprise owns and operates the server locally to execute core functions like payment processing and sales, a fixed place PE may be constituted.

- Dependent Agents and Secondments: Sending employees abroad to assist affiliates or using local intermediaries can unwittingly trigger an Agency or Service PE. Under the revised BEPS Action 7 rules, if an agent habitually plays the principal role leading to the conclusion of contracts without material modification by the foreign enterprise, a PE is established.

4. Strategic Advisory & Mitigation

Safeguarding against PE risks requires a proactive approach that prioritizes economic substance over legal form. Enterprises must evaluate their operational models holistically:

- Robust Cross-Border Regulatory Frameworks: Companies should thoroughly review intercompany agreements and employee secondment contracts. It is vital to clearly delineate roles to ensure that foreign personnel are operating under the control and supervision of the host entity rather than the parent, thereby shifting the economic employment and reducing Service PE risks. Furthermore, operations must be continuously monitored against anti-fragmentation rules to ensure cohesive business lines are not improperly structured to exploit preparatory and auxiliary exemptions.

- Transfer Pricing Alignment: Establishing a PE requires attributing profits to it under the arm's length principle. Utilizing the Authorized OECD Approach (AOA), profits must be allocated based on a rigorous functional and factual analysis of the significant people functions (SPFs) performed, the assets used, and the risks assumed by the PE. Companies must meticulously document the DEMPE functions (Development, Enhancement, Maintenance, Protection, and Exploitation) regarding any intangibles to ensure profit allocation perfectly aligns with actual value creation.

- Continuous Tax Strategy Reviews: Given the rapid implementation of the Multilateral Instrument (MLI) and evolving domestic laws, periodic reviews of local sales models are critical. Enterprises using commissionaire arrangements may need to explore transitioning to Limited Risk Distributor (LRD) models to clearly ring-fence local profit attributions and preempt tax disputes.

5. Reporting Requirements

When a permanent establishment is constituted, it activates a rigorous and layered compliance matrix within the host jurisdiction that extends far beyond corporate income tax. The foreign enterprise must immediately secure localized tax registrations, which typically include a Permanent Account Number (PAN) or Tax Deduction and Collection Account Number (TAN), alongside mandatory Goods and Services Tax (GST) or equivalent indirect tax registrations. Following registration, the enterprise is obligated to maintain separate, localized books of account and file comprehensive annual income tax returns that transparently reflect the PE’s distinct income, expenses, assets, and liabilities. The PE must meticulously fulfil all local withholding tax obligations on its incurred expenses. From a transfer pricing perspective, the compliance burden is highly substantial; the enterprise is required to prepare detailed contemporaneous transfer pricing documentation such as a Master File and Local File, participate in Country-by-Country Reporting (CbCR) to provide tax authorities with a global picture of economic activity, and frequently secure specialized accountant reports to validate that all intra-group transactions are conducted strictly at arm's length.

6. Conclusion

The identification and taxation of Permanent Establishments is no longer a static, checklist exercise; it is a highly fluid and deeply factual evaluation influenced by global digitalisation, mobile workforces, and stringent BEPS regulations. For multinational organizations, proactive PE management transcends mere compliance—it is a distinct strategic advantage. By carefully aligning operational reality with robust tax and transfer pricing policies, companies can secure their global margins and protect themselves against prolonged tax controversies.

As international tax authorities intensify their scrutiny, staying ahead of these complexities is paramount. Engaging with seasoned international tax advisors ensures that your global footprint remains structurally sound, economically efficient, and fully aligned with the latest global standards, providing your business with the clarity and confidence required to thrive across borders.

SIMILAR ARTICLES