Shares for Services: A Guide to Non-Cash Allotment for Foreign Consultants

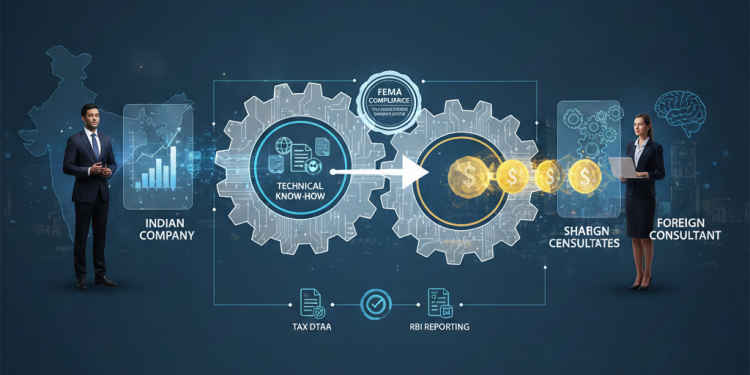

In today’s global economy, Indian companies frequently leverage international expertise to scale. When it comes to compensating these foreign consultants, many businesses explore the possibility of issuing equity shares in lieu of cash.

While this is a strategic way to manage cash flow and align interests, the regulatory landscape in India makes a clear distinction between different types of services.

Can we issue shares to a foreign consultant instead of a fee?

Generally, yes, but with specific conditions. Under Indian regulatory control guidelines, a company can issue shares against "funds payable" to a non-resident. Essentially, if you have a legal obligation to pay a consultant for services, you may be able to "capitalize" that debt into equity. However, this is primarily reserved for specific high-value contributions like technology transfers.

Does the nature of the service matter?

Absolutely. This is the most critical factor in determining if the transaction is allowed under the "Automatic Route" (without prior regulatory approval).

-

Lump-sum Technical Know-how & Royalties: If the consultant is providing technical blueprints, specialized technology, or intellectual property, the law generally allows for the issuance of shares against these dues.

-

General Consultancy & Legal Services: If the services are purely advisory, such as marketing strategy, general management, or legal counsel, the direct issuance of shares is typically not allowed without prior permission from the authorities.

What are the key tax considerations?

One cannot simply convert the total invoice value into shares. The transaction must be analyzed net of applicable taxes.

-

TDS Obligations: The Indian company must satisfy Tax Deducted at Source (TDS) requirements in cash before the equity is allotted.

-

DTAA Analysis: It is vital to review the Double Taxation Avoidance Agreement (DTAA) between India and the consultant's home country. This analysis ensures the correct tax rate is applied and prevents the consultant from being taxed twice on the same income.

Is a valuation report mandatory?

Yes. You cannot decide the share price arbitrarily. To ensure the shares are issued at a fair value, a formal valuation certification from a registered professional (such as a Chartered Accountant or a Merchant Banker) is required. This protects the company from future scrutiny regarding "undervalued" share issuances to non-residents.

What about reporting?

Even though no actual money enters a bank account, the issuance of shares is considered a "deemed" inflow. Therefore, the company must complete formal reporting with the RBI within 30 days of the allotment. This filing must be supported by the underlying service agreements and the valuation certificate.

How We Can Assist

Navigating cross-border equity issuance requires a blend of corporate law expertise and tax precision. We look forward to providing services relating to the above matter, including:

-

Classifying service agreements to meet "Technical Know-how" standards.

-

Conducting detailed DTAA and tax withholding analysis.

-

Facilitating the valuation and regulatory reporting process.

Please let us know if you would like to schedule a consultation to discuss your specific requirements.

SIMILAR ARTICLES