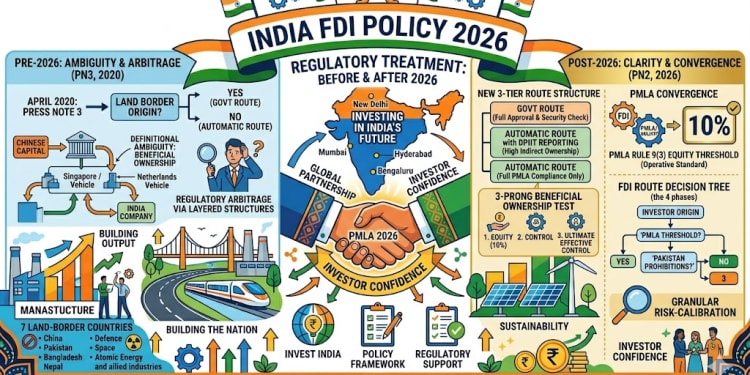

India's FDI Policy 2026: Press Note 2, Land Border Restrictions & PMLA Beneficial Ownership – Complete Guide

The Government of India's issuance of Press Note No. 2 (2026 Series) marks a structural shift in how beneficial ownership is determined for inbound foreign direct investment. For the first time, India's FDI policy explicitly cross-references and adopts the definitional framework of the Prevention of Money-laundering Act, 2002 (PMLA), setting a precise 10% equity threshold — and a qualitative control overlay — as the twin tests that determine which investment route applies.

Contents

- Background and Policy Context

- Key Numbers at a Glance

- The Four-Phase FDI Decision Tree

- Legal Mechanics of the 2026 Amendment

- Synchronisation with PMLA

- The "Ultimate Effective Control" Standard

- Secondary Transfers and Downstream Friction

- New DPIIT Reporting Paradigm

- 2020 vs. 2026: What Changed

- Practical Implications and Structuring Considerations

- Implementation Compliance Checklist

- Frequently Asked Questions

1. Background and Policy Context

India's regulatory treatment of investments originating from countries sharing a land border — China, Pakistan, Bangladesh, Nepal, Bhutan, Myanmar, and Afghanistan — has evolved significantly since the foundational change introduced by Press Note 3 (2020 Series) in April 2020. That notification, issued against the backdrop of pandemic-era concerns about opportunistic foreign takeovers, subjected all such investments to mandatory Government Route approval, replacing the prior regime under which many sectors permitted automatic entry.

The core criticism of the 2020 framework was definitional ambiguity: the concept of "beneficial ownership" was left to interpretation under general corporate law norms, creating scope for regulatory arbitrage through layered holding structures. An entity incorporated in Singapore or the Netherlands, for instance, could serve as an intermediate vehicle for Chinese capital without falling squarely within the literal terms of the restriction.

Press Note 2 (2026 Series), issued by DPIIT on 15 March 2026, closes that gap decisively. By anchoring the definition of "beneficial owner" to Section 2(1)(fa) of the PMLA and the quantitative thresholds under Rule 9(3) of the PML Rules 2005, the Government has deployed India's anti-money-laundering architecture in service of its FDI screening objectives — a significant regulatory convergence.

Key Policy Shift: For the first time, India's FDI framework expressly adopts the PMLA definition of beneficial ownership. The 10% equity threshold under Rule 9(3) — previously confined to AML/KYC compliance — is now the operative standard for determining which entry route applies to an inbound investment.

The amendment also introduces, for the first time, a specialised reporting obligation for investments that do not require Government approval but that still carry indirect ownership from a land-border country. This three-tier structure — automatic route (full compliance only), automatic route with DPIIT reporting, and Government route — reflects a more granular risk-calibration approach than the binary regime that preceded it.

2. Key Numbers at a Glance

- 10% — PMLA Rule 9(3) beneficial ownership threshold

- 7 — Land-border countries subject to restrictions

- 3 — Prongs of the beneficial ownership test (equity, control, ultimate effective control)

- 3 — Sectors prohibited for Pakistan: defence, space, atomic energy

- 4 — Decision tree phases before route is determined

3. The Four-Phase FDI Decision Tree

The following structured framework — derived directly from the amended Para 3.1.1 — should be applied in sequence by legal counsel, compliance officers, and transaction advisors whenever structuring inbound investment from or through any entity with potential land-border exposure.

Phase 1: Geographic & Entity Assessment

Question 1: Is the direct investor an entity incorporated in Pakistan, or is the investor a citizen of Pakistan?

- YES: Stop. Government Route mandatory. Investment in defence, space, and atomic energy is strictly prohibited, in addition to any sectors already prohibited for FDI generally.

- NO: Proceed to Question 2.

Question 2: Is the direct investor entity incorporated in, or is the investor a citizen of, any other country sharing a land border with India (China, Bangladesh, Nepal, Bhutan, Myanmar, Afghanistan)?

- YES: Stop. Government Route mandatory for all sectors/activities not otherwise prohibited.

- NO: Direct investor is not from a land-border country. Proceed to Phase 2 — look-through analysis.

Phase 2: Beneficial Ownership — The PMLA Threshold Test

Question 3: Do citizens and/or entities of a land-border country hold rights or entitlements — directly, indirectly, individually, cumulatively, independently or collectively — exceeding the applicable thresholds under Rule 9(3) of the PML Rules (currently 10%) over the investor entity?

- YES: Stop. Beneficial ownership is deemed vested in a land-border country. Government Route mandatory.

- NO: Land-border equity below threshold. Proceed to Phase 3 — qualitative control tests.

Phase 3: The Qualitative Control Overlay

Question 4: Regardless of equity percentage: do land-border citizens or entities possess the ability to exercise control over the intermediate investor entity — through shareholder agreements, veto rights, board appointment mechanisms, or similar instruments?

- YES: Stop. Government Route mandatory. Control, not just equity, triggers the restriction.

- NO: No control over intermediate entity. Proceed to Question 5 — ultimate effective control test.

Question 5: Do land-border citizens or entities possess the ability to exercise ultimate effective control over the Indian investee entity in any manner whatsoever — including through voting rights, management rights, economic rights, or any other mechanism at any level of the ownership chain?

- YES: Stop. Government Route mandatory. This is the broadest and most residual test.

- NO: Investment may proceed under the Automatic Route, subject to standard sectoral caps, entry conditions, and FEMA compliance. Proceed to Phase 4.

Phase 4: The DPIIT Reporting Obligation

Question 6: The investment qualifies for the Automatic Route — but does the investor entity still have any direct or indirect ownership interest held by a citizen or entity of a land-border country, even if below 10% and without control rights?

- YES: Mandatory DPIIT Reporting applies. The investment proceeds under the Automatic Route, but must be reported in the format prescribed by DPIIT's Standard Operating Procedure. This reporting is in addition to — not a substitute for — standard FEMA/FCGPR compliance.

- NO: No land-border ownership at any level. Standard FEMA/FCGPR compliance only.

Critical Note on Aggregation: The PMLA threshold test under Question 3 is applied cumulatively — the rights of all land-border citizens and entities at a given tier are aggregated. A structure in which five separate Chinese individuals each hold 2.5% of an intermediary holding company would still trigger the 10% threshold (5 × 2.5% = 12.5%) and require Government Route approval.

4. Legal Mechanics of the 2026 Amendment

The amended Para 3.1.1 operates across four sub-clauses, each performing a distinct regulatory function. Understanding the architecture of the amendment is essential to applying it correctly.

Para 3.1.1(a) — The Primary Restriction

This clause establishes the core rule: a non-resident entity may invest in India subject to the FDI Policy, except in prohibited sectors. However, an entity or citizen of a land-border country — or an investment whose beneficial owner is such a citizen — can invest only under the Government Route. Pakistan-origin investment is further restricted by an absolute prohibition on defence, space, and atomic energy, even under the Government Route.

"An entity or a citizen of a country which shares land border with India, or where the beneficial owner of an investment into India is a citizen of any such country, can invest only under the Government route." — Para 3.1.1(a), Consolidated FDI Policy as amended by Press Note 2 (2026 Series)

Para 3.1.1(b) — The Transfer Restriction

This clause extends the restriction to post-incorporation secondary transactions. Any transfer of ownership — whether of existing or future FDI in an Indian entity — that results, directly or indirectly, in beneficial ownership falling into the restricted category requires prior Government approval. This prevents regulatory evasion through buy-side acquisitions, internal corporate restructuring, or share pledge enforcement.

Para 3.1.1(c) — The Definitional Clause

This is the operative clause that delivers the 2026 amendment's central innovation. It defines "beneficial owner" with reference to Section 2(1)(fa) of the PMLA and Rule 9(3) of the PML Rules. Beneficial ownership is deemed vested in a land-border country if citizens or entities of such a country hold rights in excess of the Rule 9(3) threshold, or rights enabling control over the investor entity, or rights enabling ultimate effective control over the Indian investee entity.

Para 3.1.1(d) — The Reporting Clause

This clause creates the new intermediate compliance tier. Investments qualifying for the Automatic Route but still carrying any land-border ownership (even below the Government Route threshold) are subject to DPIIT-prescribed reporting requirements over and above standard sectoral conditions.

5. Synchronisation with PMLA: Why It Matters

The explicit linkage to the PMLA framework is the defining architectural choice of Press Note 2 (2026). It has several significant legal and practical consequences.

First, the 10% threshold is not merely a policy benchmark — it is a statutory threshold under the PMLA, subject to periodic revision through amendments to Rule 9(3). Practitioners must monitor PML Rule amendments, not just DPIIT FDI policy updates, as changes to the AML framework will automatically alter the FDI entry route calculus.

Second, the PMLA definition covers not just direct equity holders but also persons who exercise control through other means — including the right to appoint a majority of directors, the right to exercise a dominant influence over management, and partnership rights. This is a materially broader conception than the simple equity percentage analysis that characterised prior practice.

PMLA Rule 9(3) — Current Threshold: Under the Prevention of Money-laundering (Maintenance of Records) Rules, 2005, as currently in force, the applicable threshold for determination of beneficial ownership in companies is 10% of shares or capital or profits. For partnerships and trusts, different thresholds apply. Practitioners should verify the current Rule 9(3) thresholds at the time of each transaction, as these are subject to amendment by the Ministry of Finance.

Third, the synchronisation enables the use of PMLA enforcement mechanisms and evidentiary standards in FDI compliance contexts. A regulator assessing beneficial ownership for FDI purposes can draw on disclosures made under the PMLA regime, creating potential cross-regulatory information flows that structuring decisions must account for.

6. The "Ultimate Effective Control" Standard

Para 3.1.1(c)(iii) introduces the most expansive — and therefore most consequential — test in the new framework. It asks whether land-border citizens or entities have the ability to exercise "ultimate effective control over the Investee entity in any manner."

"Ultimate effective control in any manner" — the phrase is deliberately residual, designed to capture structural arrangements that satisfy the letter of the equity threshold while circumventing its purpose.

The three sequential prongs of the control analysis — (i) equity rights above the PMLA threshold, (ii) control over the investor entity, and (iii) ultimate effective control over the investee entity — are structured so that each is an independent and sufficient trigger for the Government Route. A transaction structure that is safe under prong (i) must still be evaluated under prongs (ii) and (iii).

Prong I — Equity Threshold: Rights or entitlements exceeding the Rule 9(3) threshold (currently 10%) over the investor entity, held directly or indirectly, individually or cumulatively by land-border persons.

Prong II — Investor Control: Rights enabling land-border persons to exercise control over the investor entity — regardless of equity percentage. Includes board appointment rights, veto rights, and SHA-based management rights.

Prong III — Ultimate Effective Control: Rights enabling land-border persons to exercise ultimate effective control over the Indian investee entity in any manner. The most residual and broadly drafted test.

In practice, Prong III targets shareholder agreement provisions that grant affirmative voting rights on operational matters, consent rights over capital allocation decisions, or reserved matters clauses at the investee company level. A holding structure maintaining less than 10% equity from a restricted geography but utilising aggressive contractual mechanisms to grant those restricted parties practical control over the Indian investee company will nonetheless require Government approval.

Legal counsel structuring transactions must conduct a two-level SHA review: one at the intermediary holding company level (for Prong II) and one at the Indian investee company level (for Prong III). This is a departure from prior practice, which tended to focus analysis at the level of the direct investing entity.

7. Secondary Transfers and Downstream Friction

Para 3.1.1(b) is particularly important for private equity and venture capital transactions involving secondary buyouts, drag-along/tag-along exercises, and ESOP-related share issuances at intermediate holding company levels.

The provision mandates that any transfer of ownership — whether of "existing or future FDI" — that results in beneficial ownership "falling within the restriction" requires prior Government approval. This creates several categories of transactions that may now require pre-clearance that previously operated on standard regulatory timelines.

Secondary Market Acquisitions: If a land-border country entity acquires shares in a Singapore or Netherlands holdco that in turn holds FDI in India, and that acquisition takes the land-border entity's beneficial ownership above the PMLA threshold, prior Government approval is required before the transfer completes. The obligation falls on the parties to the transfer, not merely on the Indian investee company.

Internal Corporate Restructuring: Corporate group reorganisations — upstream mergers, demergers, share-for-share exchanges — that alter the beneficial ownership profile of an intermediate holding vehicle are captured by this provision. Groups with India FDI must conduct a PMLA-threshold analysis at each tier of any planned restructuring.

Pledge Enforcement: If a land-border entity holds a pledge over shares in a non-land-border investee (as common in offshore financing structures), enforcement of that pledge — which would transfer legal title and associated rights to the pledgee — could trigger the restriction. Financing documentation for India-related structures should include representations and covenants addressing this scenario.

8. The New DPIIT Reporting Paradigm

The introduction of Para 3.1.1(d) creates a regulatory instrument that has no direct predecessor in Indian FDI policy. Investments that clear all four questions in the decision tree above — qualifying for the Automatic Route — but that still carry any quantum of land-border ownership are now subject to a specific DPIIT reporting requirement.

Several aspects of this new obligation require close attention from compliance professionals.

Scope: "Any" Direct or Indirect Ownership

The threshold for the reporting obligation is zero — any direct or indirect ownership interest held by a land-border citizen or entity triggers it. An investment by a Singapore entity in which a Chinese individual holds even 1% is subject to DPIIT reporting, even if every element of the control analysis is negative and the Automatic Route is clearly available. This is a significant compliance burden for structures with diffuse shareholding.

Format and Procedure

The reporting must be made in the format prescribed by DPIIT's Standard Operating Procedure (SOP). Practitioners should verify the current prescribed format through the official DPIIT FDI Policy portal.

Relationship to FEMA/FCGPR

The DPIIT reporting obligation is explicitly in addition to — and does not replace — existing reporting requirements under FEMA. The standard FC-GPR filing for downstream investment, and any FC-TRS filing for secondary transfers, remain mandatory alongside the new DPIIT reporting obligation.

Compliance Timing Note: The DPIIT SOP has not yet, as of this writing, specified a precise timeline for the new reporting obligation. Practitioners should monitor DPIIT's official communications and the FIRMS portal for the operative deadline. The FEMA notification date — from which the policy takes effect — is the trigger for this obligation to become operative in law.

9. 2020 vs. 2026: What Changed

| Dimension | Press Note 3 (2020) | Press Note 2 (2026) |

|---|---|---|

| Beneficial ownership definition | Not defined — left to general corporate law interpretation | Expressly defined via PMLA Section 2(1)(fa) and Rule 9(3) of PML Rules |

| Equity threshold for trigger | Ambiguous — no specific percentage prescribed | 10% (current Rule 9(3) threshold) — dynamic, tied to PML Rule amendments |

| Control analysis | Implicit — based on general principles | Explicit three-prong test: equity threshold, control over investor, ultimate effective control over investee |

| Secondary transfers | Not expressly addressed | Expressly captured — prior Government approval required for transfers shifting beneficial ownership into restricted category |

| Sub-threshold reporting | None | Mandatory DPIIT reporting for any land-border ownership, even below Government Route threshold |

| Pakistan-specific restrictions | Government Route only | Government Route only, with additional absolute prohibition on defence, space, and atomic energy |

| Regulatory convergence | FDI policy operated independently from AML framework | FDI policy expressly adopts PMLA definitional framework — creating cross-regulatory interdependencies |

10. Practical Implications and Structuring Considerations

The 2026 amendment has immediate and material consequences for several categories of transactions and ongoing corporate arrangements.

Fund Structuring and GP/LP Arrangements

Investment funds with limited partners from land-border countries must now conduct a PMLA-threshold analysis at the fund level before making India investments through an offshore vehicle. A fund with multiple Chinese LPs whose combined commitment exceeds 10% of the fund will need to route India investments through the Government Route, regardless of the fund's domicile. Existing fund structures that passed muster under the 2020 framework should be re-evaluated against the new beneficial ownership definition.

Joint Ventures with Non-Land-Border Partners

Offshore JV vehicles set up by Indian companies with non-land-border partners (for instance, a UK or US co-investor) may nonetheless include a land-border entity as a minority JV participant. If that minority participation, combined with any special rights, crosses either the equity threshold or any of the three control prongs, India investments by the JV vehicle will require Government Route approval.

Pledges and Convertible Instruments

Offshore lenders or equity investors from land-border countries holding convertible notes or warrants over intermediate holdco vehicles must assess whether conversion would take their beneficial ownership above the PMLA threshold or confer relevant control rights. Conversion clauses in such instruments may need restructuring to include condition precedents tied to Government approvals.

Existing Investments — Grandfathering Question

Para 3.1.1(b) makes clear that the restriction applies to future transfers resulting in the beneficial ownership "falling within the restriction." Existing investments that were compliant under the 2020 framework are not automatically rendered non-compliant by the 2026 amendment if no change in ownership structure occurs. However, any restructuring or secondary transfer post-amendment date must be assessed against the new framework.

11. Implementation Compliance Checklist

The following action items should be incorporated into compliance calendars and transaction checklists immediately following the operative FEMA notification date.

- Update beneficial ownership questionnaires. All investor KYC/due-diligence questionnaires for inbound FDI should be updated to specifically seek disclosure of beneficial ownership by reference to the PMLA Rule 9(3) thresholds, including at all levels of the holding chain up to the ultimate beneficial owner.

- Review existing SHA arrangements. All shareholder agreements involving India-bound investment structures should be reviewed for provisions that could confer control or effective control rights on land-border persons, triggering Prongs II or III of the beneficial ownership test.

- Audit offshore holding structures. Conduct a full beneficial ownership audit of intermediate holding companies used in India FDI structures, aggregating the interests of all land-border persons at each tier.

- Update FC-GPR filing procedures. Ensure internal procedures for FC-GPR filings are updated to include the new DPIIT reporting requirement as a parallel obligation for qualifying transactions.

- Monitor DPIIT SOP notifications. Track DPIIT official communications for the prescribed reporting format and timelines under Para 3.1.1(d).

- Monitor PML Rule 9(3) amendments. Set up a regulatory monitoring mechanism for amendments to the PML Rules, as changes to the beneficial ownership threshold will automatically alter the FDI entry route analysis.

- Review financing documentation. Review pledge and security arrangements in offshore financing structures for India-related assets to identify potential pledge-enforcement scenarios that could trigger the Para 3.1.1(b) transfer restriction.

- Update valuation and due-diligence protocols. Secondary buyouts involving India FDI require a full beneficial ownership analysis as a condition precedent to completion, with regulatory timelines for Government approval factored into transaction schedules where applicable.

- Engage the FIRMS portal. The Reserve Bank of India and the Department of Economic Affairs are integrating the new framework into the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 and the FIRMS portal. Ensure internal systems are aligned with the updated FIRMS reporting requirements.

12. Frequently Asked Questions

Does the 10% PMLA threshold apply at every level of the ownership chain?

Yes. The test is applied at the level of the "investor entity incorporated or registered in a country other than a country sharing a land border with India." This means it is applied at the immediate offshore investing entity level. However, Prong III (ultimate effective control over the Indian investee) requires analysis all the way down to the Indian company level, covering every intermediate tier in the ownership chain.

What is the consequence of failing to obtain Government approval for a qualifying transfer?

A transfer of ownership that requires prior Government approval under Para 3.1.1(b) but is completed without such approval constitutes a contravention of the FEMA and the FDI Policy. This could attract penalties under FEMA, compounding requirements, and — in serious cases — divestiture orders. The precise enforcement mechanism will be administered by the RBI and the Enforcement Directorate.

Can the DPIIT reporting obligation be satisfied retrospectively?

The SOP issued by DPIIT will specify the timelines and procedures. Until the SOP is finalised, practitioners should document and preserve all information relevant to the beneficial ownership analysis, so that the reporting obligation can be discharged promptly once the SOP is operative.

How does this interact with the automatic route for sectors like renewables or technology services?

The automatic route remains available for qualifying transactions in sectors like renewable energy or technology services, provided the beneficial ownership analysis clears all three control prongs. If a Chinese entity holds, for instance, 8% in a Singapore holdco investing in an Indian solar company without any control rights, the Automatic Route may be available — but the new DPIIT reporting obligation under Para 3.1.1(d) will apply given the sub-threshold land-border ownership.

When does the new policy take effect?

Para 2 of Press Note 2 (2026 Series) states that the decision will take effect from the date of the corresponding FEMA notification. The RBI and the Department of Economic Affairs are charged with incorporating these changes into the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019, and the FIRMS portal. The Press Note itself is dated 15 March 2026.

Disclaimer: This article is a regulatory analysis prepared for informational and educational purposes only. It does not constitute legal advice and should not be relied upon as a substitute for consultation with qualified legal counsel specialising in Indian foreign exchange law, FEMA, and FDI regulations. The regulatory position described herein is based on Press Note No. 2 (2026 Series) issued by DPIIT on 15 March 2026, and may be subject to further amendment by subsequent FEMA notifications, RBI circulars, or DPIIT clarifications. Readers are advised to verify the current regulatory position and consult professional advisors before structuring or executing any cross-border investment transaction.

Author:

Manish Harchandani

FCA | LLB | FAFD (ICAI) | DIIT (ICAI) | B. Com.

Founder — Harchandani & Associates, Chartered Accountants, Ahmedabad, Gujarat, India

SIMILAR ARTICLES