Mastering FEMA FDI Pricing Rules: Ultimate Guide to Rule 21 Compliance

1. Introduction

Foreign direct investment into India is channelled through a framework that, while structured to attract and protect overseas capital, imposes strict discipline on the pricing of equity instruments at every stage of the investment lifecycle: issuance, transfer between residents and non-residents, and exit. This discipline stems from two interlocking principles enshrined in Rule 21 of the NDI Rules 2019.

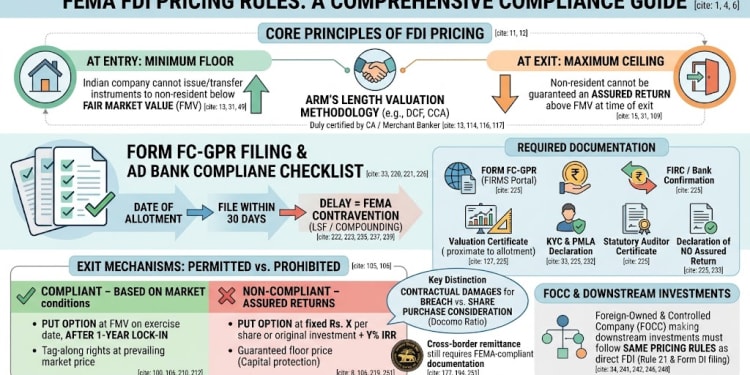

At entry: An Indian company may not issue equity instruments to a non-resident below the fair market value determined by an internationally accepted, arm's length methodology. This protects existing shareholders and the national interest from value dilution.

At exit: A non-resident investor may not be guaranteed an assured return above the fair market value prevailing at the time of exit. This ensures that FDI is genuine risk capital — participating in the company's commercial fortunes — and not a disguised debt instrument delivering a guaranteed yield.

Together, these principles mean that FDI equity pricing is fundamentally time-sensitive and market-dependent: the entry price reflects value at entry; the exit price reflects value at exit. Any contractual mechanism that pre-determines the exit price — however labelled — distorts this market-reflective structure and is impermissible under Indian law.

The practical consequences of non-compliance are severe: regulatory enforcement by the Reserve Bank of India (RBI), compounding of contraventions under FEMA, AD bank refusal to process cross-border remittances, and the unravelling of arbitral remedies at the point of cross-border transmission. Understanding the framework in its entirety — including its interface with India's BIT obligations and the jurisprudence on enforcement of foreign arbitral awards — is therefore indispensable for every legal, financial, and compliance professional engaged in inbound FDI transactions.

2. The Regulatory Architecture

2.1 Foreign Exchange Management Act, 1999

FEMA replaced the Foreign Exchange Regulation Act, 1973 (FERA) and reoriented India's approach to foreign exchange management from a penal-regulatory model to a civil-regulatory one. Under FEMA, the RBI is empowered under Section 10 to regulate the manner in which capital account transactions — including FDI — may be undertaken. The Central Government, under Section 47, is empowered to make rules relating to capital account transactions, of which the NDI Rules are the primary subordinate legislation.

2.2 NDI Rules 2019: Primary Subordinate Legislation

The Foreign Exchange Management (Non-Debt Instruments) Rules, 2019, notified by the Ministry of Finance on October 17, 2019, are the primary subordinate legislation governing FDI in equity instruments of Indian companies. The NDI Rules classify FDI-eligible equity instruments as: equity shares; fully and compulsorily convertible preference shares (FCPS); and fully and compulsorily convertible debentures (FCDs). Optionally convertible or redeemable instruments fall outside the FDI framework and are treated as debt, regulated separately as External Commercial Borrowings (ECBs).

Rule 21 of the NDI Rules contains the pricing guidelines applicable to all FDI transactions involving equity instruments. These guidelines operate as both a price floor (for issuances and resident-to-non-resident transfers) and a price ceiling (for non-resident-to-resident transfers), with separate mechanisms for listed and unlisted Indian companies.

2.3 RBI Master Direction on Foreign Investment (Updated January 2025)

The RBI has consolidated all operational directions in the Master Direction on Foreign Investment in India (MD-FI), substantially updated in January 2025. The MD-FI operationalises the NDI Rules for AD Category-I banks, prescribing documentation requirements, KYC standards, reporting timelines, and verification obligations for each type of FDI transaction. The January 2025 update confirmed that downstream investments by Foreign-Owned and Controlled Companies (FOCCs) are subject to the same pricing conditions, entry route requirements, sectoral caps, and reporting obligations as direct FDI — closing a structural gap that had been exploited in practice.

2.4 SEBI Regulations for Listed Company Pricing

For listed Indian companies, Rule 21(2) defers to SEBI guidelines. The relevant regulations are: SEBI (ICDR) Regulations 2018, Regulation 164 (preferential allotment pricing — the higher of 26-week or 2-week VWAP); SEBI (Delisting of Equity Shares) Regulations 2021 (for delisting scenarios); and the prevailing market price on a recognised stock exchange for transfers. These SEBI-mandated prices operate as a minimum for issuances and resident-to-non-resident transfers, and as a maximum for non-resident-to-resident transfers.

3. Rule 21 — Pricing Guidelines: A Granular Analysis

Rule 21 is the fulcrum of FDI pricing compliance. It governs three distinct transaction scenarios and applies specific pricing constraints to each. The following analysis addresses each scenario, together with the special provisions for equity swaps, share warrants, MoA subscriptions, and non-repatriation investments.

3.1 Issuance to a Non-Resident: Rule 21(2)(a)

When an Indian company issues equity instruments to a non-resident, the price shall not be less than:

- Listed companies: The price determined in accordance with SEBI guidelines — effectively the SEBI ICDR preferential allotment price (the higher of the 26-week or 2-week VWAP preceding the relevant date).

- Listed companies undergoing delisting: The price under the SEBI (Delisting of Equity Shares) Regulations.

- Unlisted companies: The valuation of equity instruments done as per any internationally accepted pricing methodology for valuation on an arm's length basis, duly certified by a Chartered Accountant (CA), a SEBI-registered Merchant Banker (MB), or a practising Cost Accountant.

The minimum-price rule for issuances protects existing domestic shareholders from value dilution. It ensures that when a foreign investor subscribes to new equity, the investment is at a price at least equal to what the market — or, for unlisted companies, an independent arm's length valuation — would determine.

3.2 Resident-to-Non-Resident Transfer: Rule 21(2)(b)

When a person resident in India transfers equity instruments to a non-resident, the price shall not be less than:

- Listed companies: The prevailing market price per SEBI guidelines.

- Listed companies (preferential allotment context/delisting): The applicable SEBI ICDR or Delisting Regulations price.

- Unlisted companies: The arm's length fair market value, certified by a CA, SEBI-registered MB, or Cost Accountant.

This provision prevents resident shareholders from selling equity to foreign investors at artificially low prices, which could otherwise be used to transfer value out of India in breach of FEMA's exchange control objectives.

3.3 Non-Resident-to-Resident Transfer: Rule 21(2)(c) and the Critical Statutory Explanation

This is the most significant pricing provision from a compliance standpoint. When a non-resident transfers equity instruments to a resident, the price shall not exceed:

- Listed companies: The prevailing market price per SEBI guidelines.

- Listed companies (preferential context/delisting): The applicable SEBI price, determined for the period specified in SEBI Guidelines preceding the relevant date (the date of purchase or sale of shares).

- Unlisted companies: The arm's length fair market value certified by a CA, SEBI-registered MB, or Cost Accountant.

- Equity instrument swaps: Irrespective of amount, valuation must be by a SEBI-registered Merchant Banker or an investment banker registered with the appropriate regulatory authority in the investor's home country.

- MoA subscription: At face value, subject to entry route and sectoral caps.

- Share warrants: Pricing and the conversion formula must be determined upfront.

Statutory Principle — Rule 21(2)(c)(iii) Explanation [NDI Rules 2019]"The guiding principle shall be that the person resident outside India is not guaranteed any assured exit price at the time of making such investment or agreement and shall exit at the price prevailing at the time of exit."

This Explanation is not merely aspirational. It is a statutory directive that renders impermissible any contractual provision — regardless of label — that pre-determines the exit price of a non-resident investor's equity holding. The word "prevailing" signals that the price is a function of market and valuation conditions at exit, not at entry.

3.4 Non-Repatriation Investments: The Carve-Out

The pricing guidelines under Rule 21(2) do not apply to investments in equity instruments by non-residents on a non-repatriation basis — i.e., where the principal and returns are not remittable outside India. Since such investments are not eligible for cross-border transfers of proceeds, the exchange-control rationale for mandatory arm's length pricing is absent. This carve-out underscores that Rule 21's pricing requirements are fundamentally exchange-control measures designed to protect India's foreign exchange position, not merely valuation guidelines.

4. The Arm's Length Principle: The Missing Dimension in FDI Pricing

Rules 21(2)(a)(ii), (b)(iii), and (c)(iii) each require that the valuation of equity instruments of unlisted Indian companies be conducted "as per any internationally accepted pricing methodology for valuation on an arm's length basis." The arm's length requirement is not procedural — it defines the substantive character of the price that must be determined. This is a dimension that practitioners frequently underappreciate, and which provides an independent legal basis for the prohibition on assured returns.

4.1 What the Arm's Length Standard Requires

In transfer pricing jurisprudence — where the arm's length standard has been extensively developed under Section 92C of the Income Tax Act read with the Transfer Pricing Rules — the arm's length price (ALP) is the price at which an unrelated party would transact under comparable circumstances. Three elements are essential:

- Unrelated parties: The transaction must be priced as if the parties had no common interest or control relationship.

- Comparable circumstances: The conditions of the transaction must reflect what obtains in the relevant market for comparable transactions.

- Rational economic actors: The price must be what commercially rational, well-informed, independent parties would agree to.

Applied to FDI equity pricing, the arm's length standard requires that the price of equity instruments reflect what a willing buyer and a willing seller — each with access to relevant information, each acting without compulsion — would agree upon on the transaction date. The price is time-specific, market-reflective, and commercially rational.

4.2 Why Pre-Determined Exit Pricing Is Inherently Not Arm's Length

The argument — which Rule 21's Explanation makes explicit but which is rarely articulated in this framing — is that a pre-determined exit price is, by definition, incapable of being arm's length. Four reasons support this:

- Future performance is unknowable at entry. No arm's length buyer or seller can predict what a company will be worth at a future exit date. Equity value is contingent on revenues, margins, competitive dynamics, technological change, management decisions, and macroeconomic conditions — none of which are fixed at the time of investment.

- Guaranteed minimum return converts equity into debt. An independent investor offered a minimum IRR or floor price on equity would, in economic substance, be receiving a debt-like instrument — a fixed-income claim against the company's assets. FEMA treats such instruments as debt (ECBs), subject to entirely different regulations. Dressing up a debt arrangement as equity by fixing the 'equity' exit price miscategorises the instrument and circumvents the ECB framework.

- No rational independent promoter would accept a guaranteed equity return. Under arm's length conditions, the party guaranteeing a minimum return on equity absorbs all downside risk while surrendering the upside to the investor. This is not a commercial bargain that rational, unrelated parties would strike for a genuine equity instrument.

- The transfer pricing analogy. Section 92C of the Income Tax Act disallows prices for related-party transactions that deviate from ALP — even if the parties subjectively agree to such prices. The FDI pricing framework reflects an analogous logic: the price must emerge from market conditions at the relevant date, not from a formula agreed in advance that ignores those conditions.

Practitioner's Note — Arm's Length as an Independent Ground for Non-ComplianceEven where a guaranteed return clause is structured to evade the express prohibition in Rule 21(2)(c)(iii)'s Explanation, it may independently fail the arm's length test embedded in the Rule. A valuation certifier (CA/MB/Cost Accountant) who endorses a pre-agreed fixed exit price for equity is, in substance, certifying that an arm's length transaction would yield that price — an assertion that is commercially untenable for equity instruments whose value is inherently uncertain. AD banks and the RBI are entitled to look through such certifications.

This arm's length argument is particularly powerful for cross-border related-party transactions, where the same transaction may simultaneously require an arm's length price under the transfer pricing framework (Section 92C) and under Rule 21 of the NDI Rules.

5. The Prohibition on Assured Returns: Scope, Structure, and Limits

5.1 The Statutory Basis: Three Interlocking Provisions

The prohibition on assured returns in FDI equity is established by three provisions of the NDI Rules that operate cumulatively:

- Rule 2(k)(i): "Equity instruments can contain an optionality clause subject to a minimum lock-in period of one year or as prescribed for the specific sector, whichever is higher, but without any option or right to exit at an assured price."

- Rule 9(5): "A person resident outside India holding equity instruments of an Indian company containing an optionality clause in accordance with these rules and exercising the option or right, may exit without any assured return, subject to the pricing guidelines prescribed in these rules and a minimum lock-in period of one year or a minimum lock-in period as prescribed in these rules, whichever is higher."

- Rule 21(2)(c)(iii) Explanation: "The guiding principle shall be that the person resident outside India is not guaranteed any assured exit price at the time of making such investment or agreement and shall exit at the price prevailing at the time of exit."

Read together, these provisions permit optionality (including put options) for FDI investors — but condition that optionality on: (a) a minimum one-year lock-in from allotment; and (b) exit price determination at the time of exercise in accordance with FEMA pricing guidelines, not at entry.

5.2 Compliant vs. Non-Compliant Exit Mechanisms

| ✓ Compliant — Permitted Exit Mechanisms | ✗ Non-Compliant — Prohibited Arrangements |

|---|---|

| Put option exercisable after 1-year lock-in, at FMV determined on the exercise date using DCF or CCA methodology certified by a CA or SEBI-registered Merchant Banker. | Put option exercisable at ₹X per share, or at investor's original investment plus Y% IRR per annum — exit price fixed at entry. |

| Call option for the company to repurchase investor's shares at FMV on the exercise date, per FEMA Rule 21 pricing guidelines. | "Capital protection" clause guaranteeing return of at least the original investment amount, regardless of company performance. |

| Right of first refusal (ROFR) at FMV — investor may match any third-party offer at the prevailing price determined at the time of the offer. | "Downside protection" clause ensuring investor receives not less than a floor price (e.g., 1× invested capital + 12% p.a.) at exit. |

| Tag-along rights allowing investor to sell at the same price as the promoter sells — price determined at the time of sale per market conditions. | Buy-back obligation at the higher of FMV and the original investment amount — the original investment floor creates a partial assured return. |

| Dividend on FCPS per contractual terms; interest on FCD per coupon rate — these are operational cash flows, not exit pricing. | Preferred equity return of X% per annum on invested amount, payable prior to any other distribution — likely a disguised assured return. |

5.3 Dividends on FCPS and Interest on FCDs: Not 'Assured Returns'

A frequently misunderstood boundary: dividends on FCPS and contractual interest on FCDs do not constitute 'assured returns' for the purpose of FEMA's FDI pricing rules. The prohibition targets pre-agreed fixed exit pricing on equity — the guaranteed minimum amount a non-resident receives when selling or transferring equity instruments. Normal commercial payouts arising from an instrument's contractual terms (dividends, interest) are outside the prohibition. This carve-out does not, however, extend to structuring that uses notional dividends or interest to deliver a guaranteed equity return in economic substance.

6. Valuation Methodologies: Standards, Certification, and Documentation

6.1 Internationally Accepted Methodologies

| Methodology | Description and When Most Appropriate |

|---|---|

| Discounted Cash Flow (DCF) | Projects future free cash flows and discounts to present value using a risk-adjusted discount rate (WACC). Most appropriate for companies with revenue-generating operations and reasonably predictable cash flows. The gold standard for unlisted equity valuations. |

| Comparable Company Analysis (CCA) | Values the company by reference to EV/EBITDA, P/E, or EV/Revenue multiples of publicly listed comparable companies in the same sector. Suitable where listed peers are identifiable. |

| Precedent Transaction Analysis (PTA) | Values the company based on multiples observed in recent M&A transactions in the same or comparable industries. Useful where recent deal data is available. |

| Net Asset Value (NAV) | Values the company by reference to the fair market value of its net assets (total assets minus total liabilities). Most appropriate for asset-heavy businesses, holding companies, or real estate companies. |

| Rule of Thumb / Revenue Multiple | Sector-specific multiples (e.g., X × ARR for SaaS). Acceptable as a supporting or cross-check methodology only; not as the sole method for significant transactions. |

6.2 Who Can Certify Under Rule 21

- Chartered Accountant (CA) in practice: Must hold a Certificate of Practice and be a member of ICAI.

- SEBI-registered Merchant Banker (Category I): Registered under SEBI (Merchant Bankers) Regulations 1992. Preferred for larger transactions or where SEBI interface is anticipated.

- Practising Cost Accountant: Member of ICAI (CMA) holding a Certificate of Practice.

6.3 Documentation and Retention Standards

The valuation certificate must contain: (a) the methodology adopted and justification for its selection; (b) key assumptions (discount rate, terminal growth rate, comparable multiples with sources); (c) working computations; (d) the certified fair market value per share as of the relevant date; and (e) a statement that the valuation is conducted on an arm's length basis in accordance with Rule 21. AD banks will require this certificate at the FC-GPR stage. The certificate and underlying working papers should be retained for a minimum of 5 years for potential RBI inspection.

Important: Date Proximity RequirementThe valuation must be proximate to the transaction date. While the NDI Rules do not specify a fixed maximum period, AD banks in practice apply a standard of approximately 6 months between the valuation date and the date of allotment/transfer. For exit transactions under put options, the valuation must be conducted at the time of exercise of the option — not at the time of the original investment. A valuation prepared at entry that purports to serve as the exit valuation is not FEMA-compliant.

7. Bilateral Investment Treaties: Interface with FEMA's Pricing Framework

India's bilateral investment treaty (BIT) framework operates parallel to — and at times in tension with — the domestic FEMA/NDI Rules regime. For FDI investors, understanding the BIT layer is essential both for structuring investments with adequate protection and for anticipating the available remedies when domestic regulatory compliance fails or produces arbitrary outcomes.

7.1 India's BIT Evolution: From the 1994 Template to Model BIT 2016

India signed over 80 BITs between 1994 and 2015 on the basis of a broadly worded template that provided strong investor protections: a broad Fair and Equitable Treatment (FET) standard; an MFN clause applicable to dispute settlement; no requirement to exhaust domestic remedies before invoking ISDS; and a broad definition of 'investment' covering contractual rights, portfolio holdings, and intangibles.

Following a series of adverse BIT arbitral awards — most notably White Industries v. India (2011) — and the filing of investor-state claims by Vodafone, Cairn Energy, and others, India terminated or allowed to lapse most pre-2016 BITs and published the Model BIT 2016, which substantially narrows investor protections:

| Feature | Pre-2016 BITs | Model BIT 2016 |

|---|---|---|

| FET Standard | Autonomous, broad: arbitrary, unreasonable, or discriminatory measures prohibited. | Limited to denial of justice (failure of judicial due process). General regulatory measures for public interest explicitly excluded. |

| MFN in ISDS | MFN clause could import better ISDS terms from third-party BITs. | MFN expressly limited to substantive treatment; ISDS provisions excluded from MFN scope. |

| Local Remedies | Not required; investor could proceed directly to international arbitration. | Mandatory 5-year exhaustion of domestic remedies before ISDS may be invoked. |

| Umbrella Clause | Present in many old BITs; elevated contractual obligations to treaty level. | Absent. Breach of contract is not per se a treaty violation. |

| Expropriation | Direct and indirect expropriation covered, broadly defined. | Police powers exception: regulatory measures for legitimate public purpose, non-discriminatory, proportionate — not expropriation. |

| Definition of Investment | Broad: equity, portfolio, loans, contractual rights, intangibles. | Narrowed: enterprise-based; excludes portfolio investment; goodwill/intangibles require connection to a specific enterprise. |

7.2 Key BIT Arbitrations Relevant to FDI Practitioners

A. White Industries Australia Ltd. v. Republic of India (Final Award, 30 November 2011)

The first significant BIT award against India. White Industries obtained an ICC arbitral award against Coal India Ltd. in 2002; enforcement in Indian courts took nine years. The tribunal held that India breached its MFN obligation under the India-Australia BIT by providing less effective enforcement mechanisms than those available to investors from other countries. The decision established that regulatory inaction — including prolonged delays in judicial enforcement of arbitral awards — can constitute a BIT violation independent of any deliberate regulatory hostility.

FDI pricing implication: If, following a valid foreign arbitral award related to a failed exit mechanism, the RBI systematically delays or blocks cross-border remittance without legal justification, an investor from a BIT partner country may have a cognisable BIT claim.

B. Cairn Energy PLC v. Republic of India (PCA Case No. 2016-7, Award December 2020)

Arising from India's retroactive imposition of capital gains tax on Cairn's restructuring of its Indian operations, the tribunal awarded approximately USD 1.2 billion under the India-UK BIT. India's state assets were subsequently attached in France, the UK, and the United States in enforcement proceedings. The matter was resolved in 2022 through India's repayment of the amounts collected. The case demonstrated the extraterritorial enforceability of BIT awards against sovereign assets.

FDI pricing implication: Retroactive changes to the FDI pricing framework that increase a foreign investor's fiscal burden or impair existing investments may be challenged as indirect expropriation under applicable BITs.

C. Vodafone International Holdings BV v. Republic of India (PCA Case, Award September 2020)

The tribunal found that India's attempt to apply Section 9(1)(i) of the Income Tax Act retroactively to Vodafone's acquisition of Hutchison's Indian telecommunications business violated the FET obligation under the India-Netherlands BIT. India's initial challenge to the award was unsuccessful; the matter was resolved through withdrawal of the retroactive tax demand and legislative amendment.

FDI pricing implication: Unpredictable or retroactive application of FEMA pricing rules — for example, a reinterpretation that imposes penalties on previously accepted structures — could, in principle, constitute an FET violation under an applicable BIT.

7.3 Are FEMA Pricing Rules BIT-Proof?

FEMA's pricing rules (Rule 21 of the NDI Rules) are general regulatory measures of uniform application. They apply to all non-resident investors equally, regardless of nationality. As such, they do not ordinarily constitute:

- Discrimination: All non-residents are subject to the same pricing requirements. No national treatment or MFN issue arises from the rule's text or application.

- Expropriation: The pricing rules regulate the mechanism and price of exit; they do not seize or nullify the investor's property rights. Compliance with these rules is a condition of lawful FDI, and the Model BIT 2016 explicitly protects bona fide regulatory measures from classification as expropriation.

- Denial of FET: So long as the rules are applied consistently, transparently, and with due process, no FET claim lies against the framework itself.

BIT risk can, however, arise from:

- Retroactive changes: Amending pricing rules mid-investment in a manner that substantially impairs the value of existing investments without legitimate public-interest justification.

- Arbitrary enforcement: Selective or opaque application of pricing rules by the RBI or AD banks to particular investors from specific jurisdictions.

- Cross-border remittance blocks: Systematic RBI refusal to clear remittances pursuant to a valid foreign arbitral award, without legal basis.

Structuring Insight — BIT Jurisdiction SelectionGiven India's termination of most pre-2016 BITs, foreign investors should verify whether their home country has an active BIT with India before structuring their investment. As of June 2026, India has concluded BITs with the UAE (2023), Belarus, and others under the Model BIT 2016 framework, and is negotiating new BITs with the EU and UK. Structuring investment through a jurisdiction with an active BIT provides supplementary protection, though the Model BIT 2016's narrowed FET standard and mandatory 5-year domestic exhaustion requirement substantially limit practical utility compared to pre-2016 BITs. Investors should obtain specific BIT advice from ISDS-specialised counsel before structuring.

8. Foreign Arbitral Awards: Enforcement Dynamics and FEMA Compliance

Where a foreign investor's exit mechanism fails due to promoter default, international arbitration is the commonly chosen remedy. Indian courts have developed a body of law on the intersection of foreign arbitral award enforcement, FEMA's pricing prohibition, and cross-border remittance compliance. The following cases are the most analytically significant.

8.1 NTT Docomo Inc. v. Tata Sons Ltd.

Delhi High Court | April 28, 2017 | OMP (ENF) (COMM) 7/2015

NTT Docomo had invested in Tata Teleservices Ltd. (TTSL) with a contractual right to exit at the higher of 50% of the acquisition price or fair market value. Tata Sons failed to honour the exit mechanism; an ICC arbitral tribunal in London awarded Docomo USD 1.17 billion in damages. The Delhi High Court enforced the award, holding that the payment constituted compensation for the promoter's breach of its contractual obligation — not purchase consideration for share transfer — and therefore FEMA's pricing guidelines for share transfers were not directly triggered. The RBI's objections were dismissed.

Court's Ratio — Docomo"The sum of US$1.17 billion was granted as damages and not purchase consideration for Docomo's Sale Shares; hence, pricing guidelines under FEMA for transfer of shares would not apply."

Significance: Damages for breach of a contractual exit obligation are legally distinct from the agreed exit price for a share transfer. This distinction may permit enforcement of arbitral damages even where the agreed underlying exit price would have violated FEMA's Rule 21 pricing requirements.

Docomo does not validate assured-return structures. The distinction drawn is between: (a) contractual damages for failure to implement an exit mechanism; and (b) implementation of that mechanism at a guaranteed price. If a promoter honours the agreed exit, the price must comply with FEMA; if the promoter defaults and damages are awarded, those damages — being a different legal category — may be remittable, but the cross-border remittance still requires AD bank processing and FEMA-compliant documentation.

8.2 IDBI Trusteeship Services Ltd. v. Hubtown Ltd.

Supreme Court of India | November 15, 2016 | Civil Appeal No. 10287/2016

This case arose in the context of a structured investment arrangement involving optionally convertible debentures alleged to provide fixed returns — and therefore characterised by the defendant as an ECB rather than FDI. The defendant challenged enforcement in a summary suit by raising the FEMA compliance question. The Supreme Court granted unconditional leave to defend, recognising that the FEMA characterisation of the transaction raised genuinely triable issues. The decision is frequently cited for two propositions: courts will not summarily decide complex FEMA compliance questions in enforcement proceedings; and structured investment arrangements that purport to deliver assured returns through hybrid instruments face close judicial scrutiny.

8.3 GPE (India) Ltd. & Ors. v. Twarit Consultancy Services Pvt. Ltd.

Supreme Court of India | Order dated April 17, 2023 (arising from Madras HC Judgment dated January 5, 2023)

Even after the Madras High Court upheld a foreign arbitral award relating to a put option exit mechanism, the Supreme Court directed that notice be issued to the RBI to ascertain whether any regulatory approval or permission was required for cross-border remittance of the award amount, and at what stage such approval would be required.

Key Principle — GPE v. TwaritJudicial enforcement of an arbitral award does not complete the FEMA compliance cycle. The regulatory overlay — requiring RBI clearance for the cross-border remittance of the award amount — persists at the remittance stage and is independent of the court's enforcement order. Parties must plan for AD bank scrutiny and, where necessary, direct RBI engagement before the award amount can be transferred outside India.

8.4 The Damages vs. Consideration Distinction: Analytical Framework

The emerging jurisprudence draws a legally significant line between two categories of payments:

- Pre-agreed exit price (governed by Rule 21): A payment made as consideration for the transfer of shares, calculated at a price agreed at the time of investment. This is subject to FEMA pricing guidelines and cannot be assured.

- Arbitral damages for breach (may be outside Rule 21's direct ambit): A payment awarded by a tribunal as compensation for the promoter's failure to honour a contractual exit obligation. The Docomo ratio holds that this may not be 'purchase consideration' and may therefore not directly trigger Rule 21's ceiling price for non-resident-to-resident transfers.

This distinction provides a pragmatic remedy for investors denied their contractually agreed exit. However, it does not validate the underlying arrangement: the pre-agreed price that gave rise to the breach may itself be scrutinised for FEMA compliance at the remittance stage. The prudent approach is to structure exit mechanisms to be FEMA-compliant from inception — and to plan for post-award FEMA compliance before pursuing remittance.

Post-Award Compliance Checklist

- Obtain the arbitral award and court enforcement order.

- Approach the AD Category-I bank with a FEMA-compliant remittance application, including award documentation and applicable purpose code.

- In complex cases (particularly where RBI previously raised objections), file a formal application for RBI guidance or approval before the bank processes the remittance.

- Obtain legal opinion on the tax treatment of the damages amount (capital gains vs. income) under the Income Tax Act and any applicable DTAA.

- Factor in timeline: RBI consultation can take several months and should be built into post-award planning from the outset.

9. Drafting Guidance: Agreement Clauses to Include and to Avoid

The following guidance is for legal counsel, company secretaries, investment bankers, and compliance professionals when drafting or reviewing shareholders' agreements (SHAs), share subscription agreements (SSAs), and allied FDI transaction documents.

9.1 Clauses to Include

A. FEMA Compliance Covenant (Essential in Every FDI Document)

Sample Clause — FEMA Compliance Covenant"Each party undertakes to ensure that all transactions contemplated by this Agreement are structured and consummated in strict compliance with the Foreign Exchange Management Act, 1999, the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019, and all applicable RBI Master Directions and circulars, as in force from time to time. In the event of any ambiguity as to the FEMA compliance of any particular transaction or mechanism under this Agreement, the parties shall in good faith seek regulatory guidance, including from the RBI or AD Category-I bank, before proceeding."

B. FEMA-Compliant Put Option Clause

Sample Clause — Investor Put Option (FEMA-Compliant)"Investor Put Option. At any time following the expiry of the Lock-In Period, the Investor shall have the right (but not the obligation) (the 'Investor Put Option') to require the Promoters, jointly and severally, to purchase all (but not part) of the Investor Shares at the Put Option Price.

'Put Option Price' means the fair market value of the Investor Shares, as of the Put Option Exercise Date, determined by an internationally accepted pricing methodology (including, without limitation, discounted cash flow analysis, comparable company analysis, or net asset value method, as appropriate to the nature of the Company's business at the time of exercise) on an arm's length basis, certified by a SEBI-registered Category I Merchant Banker or a Chartered Accountant in practice, in accordance with Rule 21 of the NDI Rules as in force on the Put Option Exercise Date.

For the avoidance of doubt, the Put Option Price shall not be pre-determined or subject to any minimum floor, guaranteed rate of return, minimum IRR, capital protection, or any other form of assured return. The Investor expressly acknowledges and accepts that the Put Option Price shall reflect market and commercial conditions at the time of exercise and may be higher or lower than the Investor's original investment amount."

C. Lock-In Period Clause

Sample Clause — Lock-In Period"Lock-In Period. The Investor shall not, without the prior written approval of the RBI (or as otherwise specifically permitted under applicable law), transfer, assign, sell, pledge, encumber, or otherwise dispose of any Investor Shares prior to the expiry of one (1) year from the date of allotment of the Investor Shares (or such longer period as may be prescribed for the relevant sector under the NDI Rules in force from time to time) (the 'Lock-In Period'). Any purported transfer in contravention of this Clause shall be void ab initio."

D. Independent Valuation Procedure at Exit

Sample Clause — Exit Valuation Procedure"Exit Valuation. For the purpose of determining the Put Option Price, the parties shall, within 10 Business Days of the Investor's delivery of a written Put Option Exercise Notice, jointly appoint a SEBI-registered Category I Merchant Banker as independent valuer (the 'Independent Valuer'). If the parties fail to agree on the Independent Valuer within such period, either party may request the President of ICAI (or such other agreed appointing authority) to appoint the Independent Valuer within 5 Business Days. The Independent Valuer shall deliver its final valuation report within 30 Business Days of appointment. In the absence of manifest error, the valuation so determined shall be final and binding. Costs of the Independent Valuer shall be shared equally between the Investor and the Promoters."

E. No Assured Return Representation and Warranty

Sample Clause — No Assured Return Warranty"Each party represents and warrants that: (i) it has not entered into, and shall not enter into, any arrangement, side letter, oral agreement, or understanding that has the effect of guaranteeing the Investor a fixed exit price, minimum internal rate of return, assured return, capital protection, or any similar mechanism in respect of the Investor Shares, whether by way of buy-back commitment, put option at a pre-agreed price, or otherwise; (ii) it understands that any such arrangement would be void under applicable FEMA regulations and could attract compounding proceedings and regulatory sanctions; and (iii) to the best of each party's knowledge, no such arrangement exists as of the date of this Agreement."

9.2 Clauses to Avoid: Non-Compliant Language

| Clause Type | Non-Compliant Language (Example) | Why Non-Compliant |

|---|---|---|

| IRR-Based Exit | "Investor shall be entitled to exit at a price that delivers not less than 18% per annum IRR on the Invested Amount from the date of investment to the date of exit." | Pre-determines exit price with reference to a guaranteed return. Directly violates Rule 21(2)(c)(iii) Explanation and Rule 2(k)(i). |

| Capital Protection | "The Promoters shall ensure that on any exit by the Investor, the Investor receives not less than the Invested Amount, adjusted for inflation at the CPI rate." | Guarantees minimum return equal to original investment. Constitutes an assured return regardless of 'protection' framing. |

| Floor Pricing | "The Put Option Price shall not be less than ₹[X] per share (the 'Floor Price')." | A floor price is a pre-agreed minimum exit value. Squarely prohibited as an assured exit price. |

| Fixed Buy-Back | "The Company shall repurchase the Investor Shares at ₹[X] per share on [Specific Date]." | Pre-agreed buy-back price at a fixed amount constitutes an assured exit price. |

| Hybrid Floor + FMV | "The Promoters shall purchase at the higher of FMV (per FEMA guidelines) and the original investment amount." | The FMV component alone is compliant; adding the original investment as an alternative floor creates a partial assured return — non-compliant. |

| Interest on Equity | "The Investor shall be entitled to a preferred return of 15% p.a. on the Invested Amount, payable cumulatively out of profits prior to any other distribution." | Preferred equity return at a fixed rate may be treated as a disguised assured return; also raises instrument-characterisation risk (ECB vs. FDI equity). |

10. AD Bank Compliance: FC-GPR Filing — Documents, Verification, and Best Practices

Form FC-GPR (Foreign Currency — Gross Provisional Return) is the primary regulatory filing for FDI in equity instruments. It must be filed with the RBI through the company's AD Category-I bank on the FIRMS portal within 30 days of the date of allotment. Non-filing or late filing is a contravention under FEMA 1999, subject to compounding.

10.1 Documents Required for FC-GPR Filing

| Document / Certificate | Key Details and Purpose |

|---|---|

| Form FC-GPR (FIRMS Portal) | Completed on the RBI's FIRMS (Foreign Investment Reporting and Management System) portal. Captures investee company details, foreign investor details, amount received, number and type of instruments, issue price, entry route, sector, and post-allotment foreign shareholding percentage. |

| FIRC / Bank Confirmation | Foreign Inward Remittance Certificate issued by the Indian AD bank confirming receipt of inward remittance, along with KYC certificate from the overseas bank of the foreign investor confirming source of funds. |

| KYC of Foreign Investor | Passport/incorporation documents, registered address proof, and — critically — beneficial ownership declaration per PMLA Rule 9(3) identifying any person holding 10% or more of the investing entity, or exercising effective control. Compliance with RBI KYC Master Directions and PMLA 2005 is mandatory. |

| Valuation Certificate (Unlisted Companies) | Certificate from a CA/SEBI-registered MB/Cost Accountant confirming the fair market value per share as of the allotment date, using an internationally accepted arm's length methodology per Rule 21(2)(a)(ii). Certificate must be dated proximate to the allotment date. |

| Board Resolution for Allotment | Certified copy of board resolution allotting shares/instruments to the foreign investor, specifying number, class, and issue price per instrument. |

| FIPB / DPIIT Approval (Government Route) | If the investment falls under the Government Approval Route, a copy of the relevant DPIIT approval letter must accompany the FC-GPR filing. |

| MoA and AoA | Current Memorandum of Association reflecting authorised capital and objects clause; AoA reflecting any investment-related restrictions or class-specific rights. |

| CS / Statutory Auditor Certificate | Certificate confirming: (a) allotment is in compliance with Companies Act 2013, FEMA, and NDI Rules; (b) issue price equals or exceeds Rule 21 valuation; (c) instrument is within authorised and paid-up capital; (d) entry route and sectoral cap are complied with; (e) no assured return has been extended to the investor. |

| Declaration on Absence of Assured Return | Declaration by the board of the Indian company confirming the transaction does not involve any deferred payment, guaranteed return, floor pricing, or any other form of assured return to the foreign investor. |

| SHA / SSA (if required by AD bank) | Some AD banks require submission of transaction documents for review to verify the absence of FEMA-impermissible clauses — particularly common for PE/VC investments with complex exit provisions. |

10.2 What the AD Bank Verifies: A Compliance Checklist

- Entry route: Whether the investment is on the Automatic Route or Government Route for the relevant sector and activity code (NIC 2008).

- Sectoral cap: Whether aggregate foreign investment (direct + indirect) post-allotment remains within the prescribed sectoral cap.

- Pricing compliance (Rule 21): Whether the issue price equals or exceeds the fair market value certified in the valuation report. Queries are raised where the issue price appears inconsistent with the certified value or where the methodology is not internationally accepted.

- FIRC vs. allotment amount: Whether the FIRC amount reconciles with the number of instruments issued multiplied by the issue price per instrument.

- KYC and PMLA compliance: Whether the foreign investor's identity and beneficial ownership have been established to the AD bank's satisfaction, including UBO disclosure at the 10% threshold under PMLA Rule 9(3).

- Absence of assured return provisions: Whether any SHA, SSA, or side letter presented for review contains provisions constituting an assured return. AD banks may refuse to process FC-GPR filings where such provisions are identified.

- Reporting timeline: Whether the filing is within 30 days of allotment. Late filings require a compounding application.

10.3 Reporting Timelines — Quick Reference

| Form | Trigger Event | Deadline |

|---|---|---|

| FC-GPR | Issue/allotment of equity instruments to a non-resident investor | Within 30 days of allotment |

| FC-TRS | Transfer of equity instruments between a resident and non-resident (either direction) | Within 60 days of date of receipt of consideration or date of transfer, whichever is earlier |

| Form DI | Downstream investment by an FOCC or Indian entity that has received FDI | Within 30 days of the downstream investment being made |

| Annual FLA Return | Annual return on Foreign Liabilities and Assets | By 15th July each year for the preceding financial year |

| FCGPR (B) | Capitalisation of import payables or foreign currency loans as equity | Within 30 days of allotment pursuant to capitalisation |

10.4 Common AD Bank Queries and Recommended Responses

| Common Query / Issue at FC-GPR Stage | Recommended Action / Best Practice |

|---|---|

| Valuation date too remote from allotment date (more than ~6 months) | Obtain a fresh valuation certificate. Provide a covering letter explaining that the business has not materially changed between the valuation date and allotment date, with supporting financial evidence. |

| Issue price below certified FMV | Not permissible. Review the valuation and re-issue at a price at least equal to the certified FMV. If there is a genuine methodology dispute, obtain a second opinion from a SEBI-registered Merchant Banker. |

| SHA/SSA contains IRR formula, floor pricing, or 'downside protection' language | Amend the offending clauses before filing. File the clean amended version. Provide a board declaration that no assured return exists. In egregious cases, the AD bank may require a legal opinion. |

| Foreign investor is a fund/trust structure with a complex UBO chain | Provide a detailed beneficial ownership chart identifying all UBOs at the 10% threshold. For funds, obtain a UBO certificate from the fund administrator. PMLA compliance documentation from the overseas bank may also be required. |

| Investment in a sector with unclear entry route (Government vs. Automatic) | Obtain a formal DPIIT clarification or Senior Counsel opinion before filing. Present it to the AD bank with the FC-GPR documents. |

| Delay in filing beyond 30 days | File a late FC-GPR with a compounding application to the RBI's regional office. Prepare a detailed reason for delay with supporting documentation. Engage qualified FEMA counsel for compounding proceedings. |

11. FOCC and Downstream Investment Compliance

A significant structuring risk arises when a Foreign-Owned and Controlled Company (FOCC) — an Indian company owned or controlled by non-residents — seeks to make downstream investments in other Indian companies on terms that include assured return elements, on the misapprehension that FEMA's pricing constraints apply only to direct FDI flows.

The RBI's January 2025 update to the Master Direction on Foreign Investment closed this loophole definitively: downstream investments by FOCCs are to be treated at par with direct FDI in all material respects — entry route, sectoral caps, pricing conditions, conditionalities, and reporting. Any assured-return structure that is impermissible for direct FDI is equally impermissible when introduced at the FOCC downstream level.

Key compliance obligations for FOCC downstream investments:

- Form DI: Must be filed by the FOCC on the FIRMS portal within 30 days of making the downstream investment.

- Pricing: The consideration for the downstream investment must satisfy Rule 21 pricing requirements — arm's length valuation for unlisted companies.

- Entry route: The more restrictive of the FOCC's own entry route and the downstream sector's entry route applies.

- No assured returns at downstream level: Any FCPS or FCD issued by the downstream Indian entity to the FOCC must not carry assured return terms that would be impermissible if the investment were made directly by the non-resident parent.

- Indirectly held FDI: For purposes of computing aggregate foreign investment in the downstream company, both direct FDI and indirect FDI held through the FOCC are counted.

12. Frequently Asked Questions

Q1. Are dividends on FCPS or interest on FCDs treated as 'assured returns'?

No. Dividends on FCPS and contractual interest on FCDs are normal commercial payouts arising from the instrument's terms. They are not treated as 'assured returns' under FEMA. The prohibition covers pre-agreed fixed exit pricing on equity instruments, not operational cash flows from the instrument's contractual structure.

Q2. Can a put option clause say "at the higher of FMV or original investment amount"?

No. The FMV limb alone is FEMA-compliant. Adding the original investment amount as an alternative floor creates an assured minimum return — non-compliant. The option must simply provide for exit at FMV determined at the time of exercise per FEMA pricing guidelines.

Q3. If the promoter breaches the exit obligation, can the foreign investor recover damages?

Yes, per the Docomo ratio: damages awarded by a tribunal for the promoter's failure to honour a contractual exit obligation may be enforced by Indian courts, because they are compensation for breach and legally distinct from share purchase consideration. However, cross-border remittance of damages still requires AD bank processing and, in complex cases, RBI consultation. Judicial enforcement of the award does not, by itself, complete the FEMA compliance cycle.

Q4. Does a BIT protect my investment against FEMA pricing restrictions?

FEMA pricing rules are general regulatory measures of uniform application and are unlikely to constitute expropriation or FET violation under India's BITs. However, retroactive changes to pricing rules, discriminatory enforcement, or unjustified blocking of cross-border remittances after a valid arbitral award could give rise to BIT claims under the applicable treaty. Verify whether your home country has an active BIT with India before structuring your investment, and obtain ISDS-specialised legal advice.

Q5. Can optionally convertible instruments (OCDs, OCPS) be used for FDI equity to deliver a fixed return?

No. Optionally convertible instruments are classified as debt under the NDI Rules and regulated as ECBs. Using an optionally convertible instrument to deliver a fixed return on what is presented as FDI equity is an impermissible circumvention of Rule 21 pricing requirements and may constitute a FEMA contravention. If a fixed return is the commercial objective, structure the investment as an ECB and comply with the applicable ECB framework.

Q6. What happens if FC-GPR is filed late?

Delayed filing of Form FC-GPR constitutes a violation of FEMA regulations. If the delay is within a certain permissible window, it can be regularized by paying a Late Submission Fee (LSF). However, if the delay exceeds this limit, the company must submit a compounding application to the relevant regional office of the RBI under Section 15 of FEMA. Compounding fees are calculated based on the transaction value and the duration of the delay. It is highly recommended to engage a qualified FEMA consultant immediately; notably, voluntary disclosure prior to RBI detection generally results in more favorable treatment.

13. Conclusion

India's FDI pricing framework under Rule 21 of the NDI Rules 2019 is comprehensive, coherent, and strictly enforced. Its organising principle — that the exit price of a non-resident investor's equity must be determined by the market at the time of exit, not by a pre-agreed formula at the time of entry — is not merely a regulatory requirement. It reflects a fundamental economic logic: equity instruments, by their nature, carry business risk. Any arrangement that eliminates that risk through a pre-agreed return converts the substance of the instrument from equity to debt, which is regulated differently and for good reason.

The arm's length requirement embedded in Rule 21 provides an additional and independent legal ground for the prohibition on assured returns — a dimension that practitioners have largely overlooked. No arm's length transaction between unrelated parties would involve a guaranteed minimum return on equity, because such a guarantee transfers all downside risk to the Indian promoter while preserving the upside for the foreign investor. This is not a bargain that rational, independent parties would voluntarily accept for a genuine equity instrument, which is precisely why FEMA does not permit it.

The BIT framework adds a further strategic dimension: while FEMA pricing rules are generally BIT-proof as non-discriminatory regulatory measures of general application, retroactive changes, arbitrary enforcement, or systematic blocking of post-award remittances could attract treaty claims under applicable BITs. The Docomo, IDBI Trusteeship, and GPE v. Twarit decisions collectively establish that the enforcement journey for a foreign investor who has been denied an exit is long and complex — and does not end with a court order. FEMA compliance at the remittance stage persists as an independent regulatory obligation.

The practical takeaways are clear: draft exit mechanisms with FMV-at-exercise, not pre-agreed prices; obtain contemporaneous arm's length valuations from qualified professionals; file FC-GPR within 30 days with complete documentation; apply FOCC downstream investments with the same rigour as direct FDI; and plan post-arbitral-award FEMA compliance well before attempting cross-border remittance. The discipline imposed by India's FDI pricing framework is, ultimately, a structural feature and not an obstacle: it ensures that FDI in Indian equity is genuine risk capital — participating in the fortunes of Indian enterprises — and not a disguised form of debt arbitrage that depletes domestic value while manufacturing a veneer of equity investment.

Disclaimer: This article is intended for informational and educational purposes for legal, financial, and compliance professionals. It does not constitute legal advice and should not be relied upon as such for any specific transaction. Specific FDI transactions should be reviewed by qualified FEMA counsel and, where appropriate, ISDS-specialised practitioners.

Manish Harchandani | CA | LLB | FAFD (ICAI) | DIIT (ICAI) | Founder, Harchandani & Associates, Ahmedabad

SIMILAR ARTICLES